Home Buyer's Guide to Closing Costs in North Carolina

Are you thinking of buying a home in North Carolina? If so, you'll want to be aware of the closing costs involved. Closing costs are the fees and expenses that you pay when you purchase a home, so it's important to know what to expect before you begin the home buying process.

In this comprehensive guide to closing costs in North Carolina, you’ll learn exactly how much you can expect to pay and what these closing costs cover. So whether you're a first-time home buyer or an experienced seller, stay tuned, because we’re going to tell you everything you need to know.

Table of Contents:

Chapters

How Much Are Closing Costs?

In 2021, the national average for closing costs was $6,905, or 1.3% of the average total sales price, but closing costs can change drastically from state to state. In Washington D.C., for example, home buyers pay as much as 3.9% of the total sales price, while closing costs in Missouri are only 0.9%.

Fortunately, North Carolina's closing costs come in slightly below the national average at just 1.1% of the sales price. So, if your dream house closes at $300,000, you can expect to pay $3,300 in closing costs.

But what do these costs entail, anyway? Here is a quick list of some of the fees and taxes that we will cover a little bit later:

-

Title fees

-

Home appraisal fees

-

Home inspection fees

-

Transfer tax

-

Homeowner's insurance fees

-

Escrow fees

-

Loan origination fees

Closing Costs in North Carolina

So you’ve found your dream home in the Tar Heel State and submitted your offer. Now it’s time to cover the closing costs.

In North Carolina, the buyer and seller are both responsible for a portion of the closing costs, but that doesn’t mean there isn’t any wiggle room.

In fact, a savvy buyer may even be able to negotiate with the seller to cover a portion of the costs. This is more common when the seller is eager to sell but can be a helpful bargaining tool in the negotiation process.

Additionally, if you are taking a loan to purchase the home, you may be able to ask your lender to cover the closing costs. Lenders do this from time to time as an incentive to get people to take out loans with them, which, unfortunately, means you'll be paying a premium for the convenience.

Who Pays Closing Costs in North Carolina?

In North Carolina, both the buyer and the seller can expect to pay a portion of the closing costs.

Generally, the closing costs for the seller include things like transfer taxes and other administrative fees, while the closing costs for the buyer in North Carolina include fees involving the transfer of the deed and things like the appraisal, inspection, and insurance fees.

That said, every real estate purchase is different., That’s why it's always best to consult with your real estate agent or closing attorney to get an estimate of what you can expect to pay in closing costs. You may even be able to convince the seller to cover all the costs!

|

Closing Costs In NC for the Buyer Estimates based on the average price of a home ($320,000) in NC |

|

|

Home Appraisal Fee |

$300-400 |

|

Home Inspection Fee |

$300 |

|

Title Fee |

$300-600 |

|

Title Insurance Fee |

$800 (up to 0.25% of the total sale price) |

|

Homeowner’s Insurance Fee |

$1,700 per year |

|

Escrow Fee |

Varies |

|

Loan Origination Fee |

$800 (capped at 0.25% of the total sale price) |

|

NC Closing Costs for the Seller |

|

|

Transfer Tax |

$600 |

|

Excise Tax |

Varies from country to county |

|

Escrow Fee |

Varies |

|

Realtor Commission |

5.6% |

|

Mortgage Payoff |

Varies |

Title Fees

One aspect of closing costs is the title fees. Now, there are two separate types of title fees: title search and title insurance fees.

A title search is the examination of public records to determine the legal history of a property and confirm the seller’s ownership. The title search verifies that the current owner is not behind on taxes or dealing with any ongoing lawsuits that may impact the seller.

A settlement agent handles this process, though individuals can initiate a title search as well. The buyer typically pays for the title search and can expect to pay anywhere between $300-600.

Title insurance, while optional, is a valuable tool that could protect you and your lender against any unforeseen problems with the title transfer. It’s a one-time expense paid by the buyer. The cost in North Carolina generally sits between 0.22%–0.25% of the purchase price of the home. This means you could expect to pay up to $750 on a $300,000 purchase.

The final step for buyers in the title process is to have the new deed recorded in the county’s records. This will require the buyer to pay a one-time recording fee. The recording fee in North Carolina varies by the property’s county. This costs around $26 for the instruments and $64 for the deeds of trust and mortgages.

Home Appraisal Fee

The home appraisal fee is another closing cost that is the buyer’s responsibility.

Appraisals are done by a third party and are a valuable asset in determining the true value of the home you’re looking to buy.

Imagine you were interested in purchasing a house on the market for $300,000, but the independent appraiser valued it at just $250,000. That would give you some major negotiating power, and could potentially save you a whole lot of money!

The total cost for a home appraisal fee can range between $300 and $400 for a single-family home, though the costs could increase slightly in a multi-family home due to size and other factors.

Home Inspection Fee

A home inspection is another cost that is well worth it for a buyer.

Independent home inspectors check the property’s integrity — from the foundation and plumbing to the electrical wiring and roofing. Not only can it save you heaps of cash in the long run, but it may also keep you and your family safe.

Inspectors identify and estimate the costs of potential problems with some of the most important infrastructure in the property you’re looking to call home. Inspectors will typically look at the following:

-

Foundation

-

Gas and water lines

-

Heating and central air conditioning

-

Roof and rainwater management

-

Attic and insulation

-

Water heater

-

Basement

This means you can negotiate with the seller to fix any problems that might arise or potentially subtract these costs from your purchase price.

Though not everyone gets a home inspection, it is highly recommended. Considering home inspection fees average around $300 in North Carolina, it’s a small price to pay to protect yourself against potential structural problems that could cost thousands — if not tens of thousands — of dollars to repair.

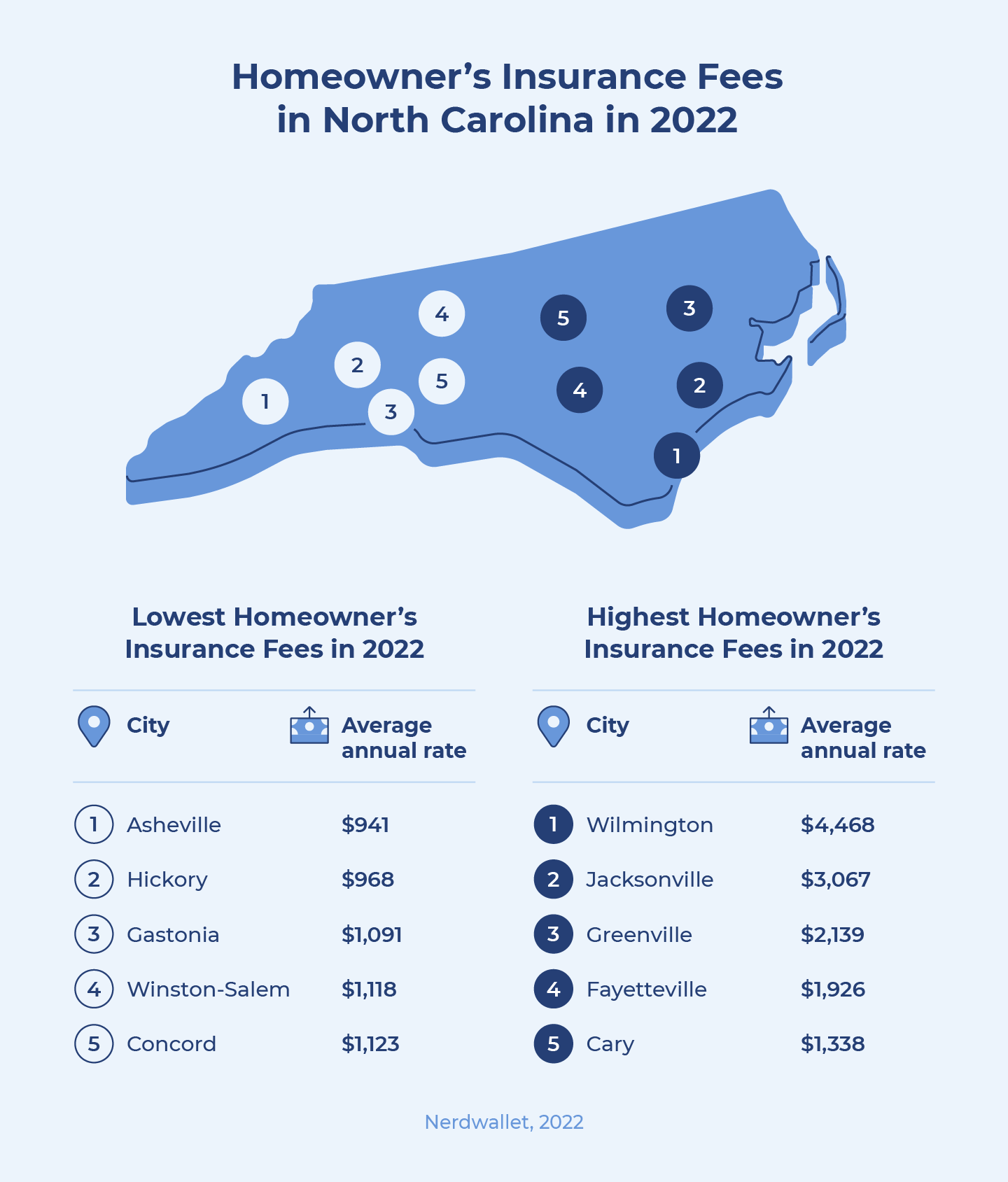

Homeowner’s Insurance Fee

Homeowner’s insurance is another seller’s closing cost when purchasing a new house.

While almost everyone expects to pay for insurance on a monthly basis, some may forget that many lenders require a year of payment upfront. This could come as an unexpected extra cost to some.

Monthly homeowner’s insurance payments in North Carolina average around $1,700 per year, or $142 per month, though a number of factors impact this.

Because of overall location and proximity to the ocean, homeowner’s insurance fees may be much higher in some cities. For example, the coastal metropolis of Wilmington carries a yearly homeowner’s insurance cost of nearly $4,500 on average. On the other hand, homeowners in Hickory — located much further inland — can expect to pay just under $1,000 per year.

Despite the costs, homeowner’s insurance is an absolute necessity. Not only will this protect your investment from nature’s wrath, but it’s also often required if you’re paying for your home with a mortgage.

Transfer Tax

Transfer taxes are a tricky beast. In North Carolina, transfer taxes can be charged by the state, county, and city, or even all three. In fact, there are even seven counties that impose an additional excise tax when a property is sold. Those counties are…

-

Camden

-

Chowan

-

Currituck

-

Dare

-

Pasquotank

-

Perquimans

-

Washington

While the rates of each county’s excise tax vary, the amount in some cases can reach up to 1% of the home sale price. This means that if you purchase a $300,000 property in one of these seven counties, you may fork out out as much as $3,000 in additional taxes. That’s a pretty significant chunk of change compared to the typical transfer tax of $640 paid in other counties.

Don’t worry, though. As a buyer, you aren’t generally expected to pay this tax.

Closing Costs with a Mortgage

Now that you know what to expect from both a buyer's and seller's perspective, let's move on to the specific closing costs with a mortgage. If you’re a cash buyer in NC, you can skip this section, as many of these fees do not apply to you.

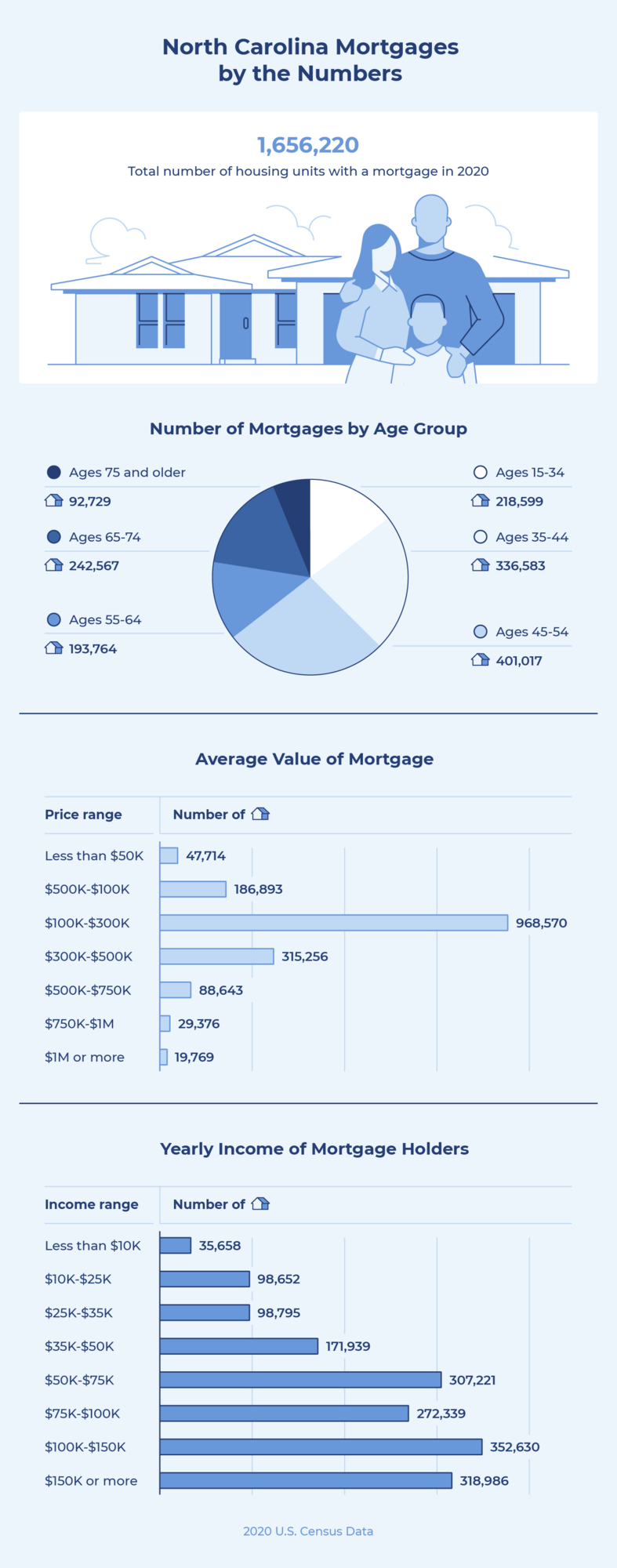

U.S. Census data estimates that that are more than 1.6 million housing units in the state of North Carolina with a mortgage, while just under 1 million are mortgage-free.

Here is a quick look at some other important North Carolina mortgage statistics:

While you may already have your downpayment tucked away and you’ve estimated your monthly mortgage payments, you might not be aware that your lender often charges a fee for preparing this loan. In fact, this fee can reach as high as 2% of the total mortgage value. This means you should pick your lender wisely!

Escrow Fees

There are a number of different types of escrow accounts available to homebuyers.

The most common escrow account homebuyers encounter is set up by lenders to collect yearly tax and homeowner’s insurance payments. This allows buyers to make monthly payments that the lender pays out at the end of every year. Many homeowners find it easier to pay into an escrow account monthly over making larger payments once a year.

Other funds that could be held in escrow accounts include:

-

Deposits

-

Down payments

-

Title insurance

-

Attorney fees

-

Holding and distribution fees

-

Private mortgage insurance

-

Realtor fees

Because there are so many types of escrow accounts, the escrow fees can vary dramatically.

Loan Origination Fees

Loan origination fees are fairly simple. They are the fees charged when a mortgage lender processes your loan application. And in 2019, North Carolina put a hard cap on how much lenders could charge.

The amendment says that lenders can only charge 0.25% of the principal amount of a loan of $100,000 or higher.

While negotiating the loan, buyers should also be aware of “mortgage points” or “discount points.”

These points are an upfront cost that a buyer can optionally pay to a lender, possibly reducing the total amount of interest paid on the loan. The process can be complicated, and the amount of interest each point reduces can fluctuate from financial institution to financial institution, or even over the course of your loan.

Each point you purchase costs 1% of your principal amount, but the savings can truly add up. Speak to your lender to determine whether purchasing points is a good investment for you.

FAQs

Who Pays Closing Costs in North Carolina?

Both the buyer and seller are responsible for paying closing costs in North Carolina. Some of these costs can be negotiated, so ask your realtor to determine where you may be able to save some extra money.

Who Pays the Transfer Tax in North Carolina?

The seller is responsible for paying the transfer tax in North Carolina. Though this costs around $640 on average, there are sometimes extra excise taxes levied on the seller depending on the county.

Is North Carolina a Buyer Beware State?

North Carolina is a buyer beware state. This means you need to always do your own research when you are purchasing a new home. Do not skip things like inspection fees, title searches, or appraisal fees, because it could lead to some serious problems.

Are You Ready To Close On Your New House?

Now you should have a better idea of exactly what to expect when buying a new home in Raleigh. A real estate attorney is required to be at closing, and closing costs in North Carolina can be overwhelming, but we’re here to support you on this incredible journey to the City of Oaks.

Raleigh Reality is here to answer any questions you might have about buying your dream home in Raleigh.

Ryan Fitzgerald

Hi there! Nice to 'meet' you and thanks for visiting our Raleigh Real Estate Blog! My name is Ryan Fitzgerald, and I'm a REALTOR® in Raleigh-Durham, NC, the owner of Raleigh Realty. I work alongside some of the best Realtors in Raleigh. You can find more of my real estate content on Forbes, Wall Street Journal, U.S. News and more. Realtor Magazine named me a top 30 under 30 Realtor in the country (it was a long time ago haha). Any way, that's enough about me. I'd love to learn more about you if you'd like to connect with me on Facebook and Instagram or connect with our team at Raleigh Realty. Looking forward to connecting!